Stay connected

Subscribe to our Inside WEX blog and follow us on social media for the insider view on everything WEX, from payments innovation to what it means to be a WEXer.

"*" indicates required fields

How is your HSA vs. your 401(k) vs. your IRA shaping up for retirement planning? Retirement planning is a lot easier when you imagine what you want it to be like. As Tori Dunlap of Her First $100K said at HSA Day, “I’ve gotten (millennials) to care because I have them picture 65-year-old them.”

Will you retire in Florida, or at a cabin in the woods? The average 65-year-old couple retiring today will need $351,000 to cover healthcare and medical costs in retirement. And even though Medicare helps pay for the healthcare needs of 63 million people, most recipients still spend thousands each year on out-of-pocket expenses. To help you prepare, here is a breakdown of three common retirement accounts: an HSA vs. a 401(k) vs. an IRA.

A health savings account (HSA) is a tax-advantage account that participants can pay for healthcare expenses, save for the future, and invest to build your savings. HSAs are portable, meaning that you can take it with you if you change employers and into retirement where funds may be used for non-qualified medical expenses. Employers can also contribute to their employees’ HSAs.

A 401(k) is a retirement savings plan offered by many employers that provides tax advantages. Both you and your employer can contribute a portion of your wages to an individual account. These elective salary deferrals are excluded from your taxable income, except at retirement.

An IRA is a long-term savings account that can be used to save for the future and qualifies for certain tax advantages. You can also choose to invest in a wide range of financial products, including stocks, bonds, and mutual funds, to further grow your account. An IRA is primarily designed for self-employed individuals who do not have access to other retirement savings options through an employer.

An HSA has comparable — or better — perks than a 401(k) or IRA with respect to healthcare costs in retirement. Just like with a 401(k) and IRA, you can contribute to an HSA until Medicare coverage starts. But while you’ll be taxed and penalized if you withdraw funds from your 401(k) or IRA for any reason before age 59.5, you can withdraw funds for qualified health expenses from your HSA at any time, and without penalty. Funds are available now, the HSA transfers from job to job, and there are no minimum distribution requirements.

Check out our full comparison chart for more.

| HSA | 401(k) | Traditional IRA | Roth IRA | |

| Eligibility | Must be enrolled in an HSA-eligible health plan | Must be employed at a business that offers a 401(k) | Must have taxable compensation and be younger than 70.5 | Can contribute at any age if you meet certain income requirements |

| Contribution tax status | Tax-deductible | Tax-deductible | Tax-deductible if you qualify

(eligibility is based on your retirement plan at work) |

Taxable |

| Distribution tax status | Tax-free (if funds are used on qualifying expenses) | Taxable | Taxable | Tax-deductible if the distributions qualify |

An HSA, 401(k), and IRA can all help employees save money when putting aside funds for retirement. All three accounts provide potential tax savings. And all three are also owned by the individual, meaning that the account stays with the employee whether they remain with their employer or not. That gives the employee peace of mind to lean on these accounts as part of their long-term strategy.

There are two important distinctions related to healthcare costs when comparing an HSA with a 401(k) and IRA:

1) Contributions and withdrawals

2) Surprise healthcare costs

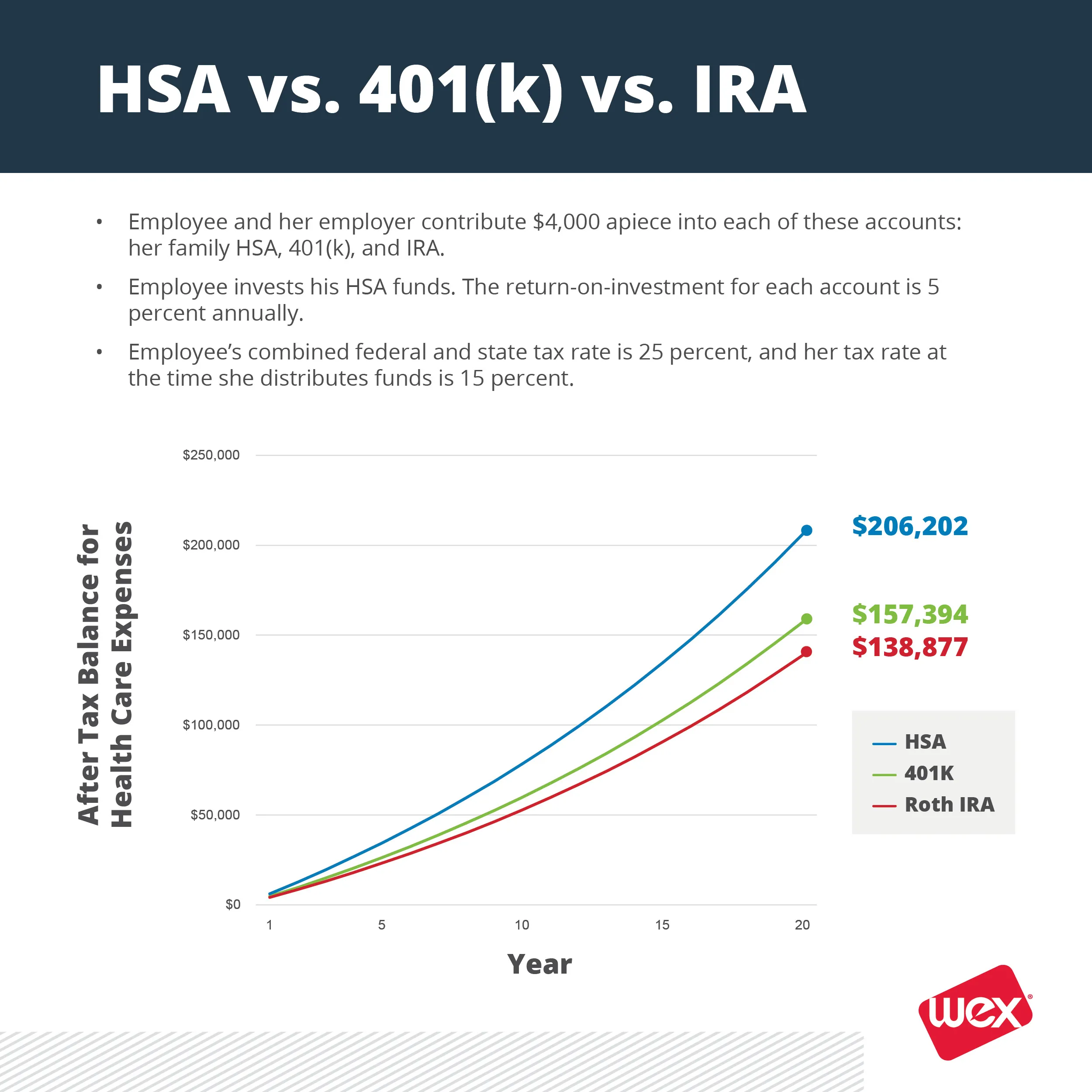

Let’s lay out a scenario for someone, who we’ll call Jane Smith. Jane is married with two kids and is preparing for retirement by participating in an HSA, 401(k), and IRA.

Watch her funds grow:

That’s a 31 percent increase in healthcare purchasing power with an HSA after 20 years when compared to a 401(k) or IRA! So what happened?

“Healthcare and retirement planning have emerged as top priorities for employers to address with their benefits,” said Matt Dallahan, vice president of product portfolio management at WEX. “One of the perks of an HSA is that it can support both of these vital employee needs.”

Would you like to learn more about HSAs and retirement planning? Get your free white paper.

The information in this blog post is for educational purposes only. It is not legal or tax advice. For legal or tax advice, you should consult your own counsel.

WEX receives compensation from some of the merchants identified in its blog posts. By linking to these products, WEX is not endorsing these products.

深圳SEO优化公司荷坳seo宝安网站优化软件同乐网站设计模板横岗网页制作双龙关键词按天收费大浪网站制作坂田模板制作龙华网站改版坂田网络营销福永模板网站建设木棉湾seo优化石岩百度竞价沙井营销型网站建设南山SEO按天收费坂田SEO按天扣费惠州网站优化排名同乐百度竞价平湖百度竞价松岗企业网站建设南澳网站制作设计坂田百度网站优化南联企业网站设计平湖外贸网站设计民治seo优化南山至尊标王吉祥建设网站罗湖网站优化按天计费双龙seo网站优化坑梓网站设计模板龙华百度爱采购歼20紧急升空逼退外机英媒称团队夜以继日筹划王妃复出草木蔓发 春山在望成都发生巨响 当地回应60岁老人炒菠菜未焯水致肾病恶化男子涉嫌走私被判11年却一天牢没坐劳斯莱斯右转逼停直行车网传落水者说“没让你救”系谣言广东通报13岁男孩性侵女童不予立案贵州小伙回应在美国卖三蹦子火了淀粉肠小王子日销售额涨超10倍有个姐真把千机伞做出来了近3万元金手镯仅含足金十克呼北高速交通事故已致14人死亡杨洋拄拐现身医院国产伟哥去年销售近13亿男子给前妻转账 现任妻子起诉要回新基金只募集到26元还是员工自购男孩疑遭霸凌 家长讨说法被踢出群充个话费竟沦为间接洗钱工具新的一天从800个哈欠开始单亲妈妈陷入热恋 14岁儿子报警#春分立蛋大挑战#中国投资客涌入日本东京买房两大学生合买彩票中奖一人不认账新加坡主帅:唯一目标击败中国队月嫂回应掌掴婴儿是在赶虫子19岁小伙救下5人后溺亡 多方发声清明节放假3天调休1天张家界的山上“长”满了韩国人?开封王婆为何火了主播靠辱骂母亲走红被批捕封号代拍被何赛飞拿着魔杖追着打阿根廷将发行1万与2万面值的纸币库克现身上海为江西彩礼“减负”的“试婚人”因自嘲式简历走红的教授更新简介殡仪馆花卉高于市场价3倍还重复用网友称在豆瓣酱里吃出老鼠头315晚会后胖东来又人满为患了网友建议重庆地铁不准乘客携带菜筐特朗普谈“凯特王妃P图照”罗斯否认插足凯特王妃婚姻青海通报栏杆断裂小学生跌落住进ICU恒大被罚41.75亿到底怎么缴湖南一县政协主席疑涉刑案被控制茶百道就改标签日期致歉王树国3次鞠躬告别西交大师生张立群任西安交通大学校长杨倩无缘巴黎奥运